What, however, are the factors driving this downward price trend and what are the impacts on the food sector environment and, in particular, the meat sector?

An imbalance in oil supply and demand is the main driving force behind the drastic fall in prices over the second half of 2014. With prices up by more than US$100 per barrel for an extended period, there is structural oversupply, with many of the major oil-producing countries refusing to scale back their production to ease the situation.

In the US, oil production has been at its highest point for almost 30 years. Russian producers do not want to reduce their volumes for fear of losing their markets to competitors. Meanwhile, the Saudi Arabian industry believes it is able to withstand lower prices, and is encouraged as it hopes this will enable it to out-compete higher-cost producers from the market.

On the demand side, poor economic growth within many major oil importing countries, such as China and the EU 28, has resulted in weak demand levels, further exasperating the issue of increased supply volumes. This situation is akin as to what is happening in global food sectors, such as dairy.

Here, a number of high volume countries, such as the EU 28, the US and New Zealand, increased their production in 2014, only to see demand fall away in major import markets, such as China and Russia (albeit for different reasons). The result of this has been an imbalance in supply and demand, leading to rapidly falling global milk prices. As such, the oil and food sectors have a strong link. This is discussed further on.

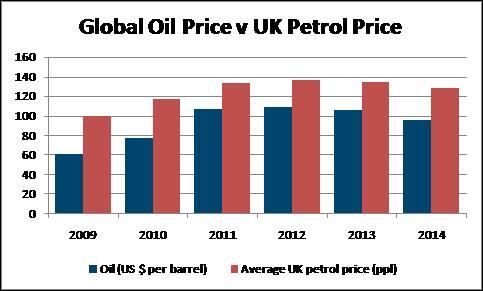

The volatility being witnessed in the oil sector has some potential positives for the meat supply chain, however. One of the most highlighted in the UK media is the effect it is having on petrol prices. Figure 1 below shows how the rise and fall of oil prices correlates with the UK average petrol price trend.

Figure 1: Global Oil Price v UK Petrol Price

Source: OPEC, and Petrolprices.com

At a domestic level, lower fuel prices, coupled with lower energy costs, mean a potential increase in consumers’ disposable income. Latest Defra statistics show that UK consumers spent £196 billion on food and drink. This works out an average of £3,058 per person, or just under £60 per person per week. A typical consumer in the UK now spends just under 12% of their household budget on food and drink, but with lower-income households spending close to 17%. Price is still often one of the most important factors influencing consumer food purchase decisions, according to IGD research.

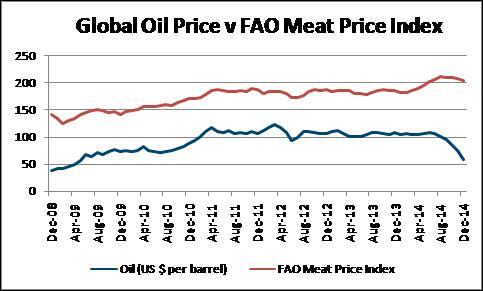

There looks to be a strong correlation when comparing the oil price and the FAO meat price index, as highlighted in Figure 2 below. Over the second half of 2014, the meat index dropped notably, although at a lower rate than the oil price, as there is a time lag between the oil price and the impact this has on food and meat prices, in particular. As such, with greater disposable income, and potentially lower food prices, this could be a "win win" situation for consumers, retailers and the foodservice sector alike

Figure 2: Global Oil Price v FAO Meat Price Index

In any volatile market situation, there are going to be winners and losers. The impact of the dramatic price fall in the oil sector should eventually work its way down the supply chain and, hopefully, result in lower food prices for the end-consumer – whether it works this way in practice though is another question. We shall have to wait and see.

In theory, a fall in oil (prices) should result in a domino effect of other falling prices: energy, packaging and transport costs for processors in energy-intensive meat processing factories and lower energy, fertiliser and transport costs for farmers alike, all combining to produce a general easing of pressure in the food and meat industry. This is good news for processors and farmers and eventually consumers, we hope, but less good for oil companies.

Consumers are already demanding greater transparency from the petroleum industry to understand how the oil price will impact on prices at the pump.

In the meat and wider food industry, however, the real question is if, and when, this downward trend will make its way onto supermarket shelves and also give a much-needed boost to the UK and international farming and meat processing sectors. Energy, transport and packaging costs are all important contributors to the make-up of the cost chain, but there are others to take into account – not least human, other physical and financial resources.

Greater transparency within the food supply chain is needed in order for suppliers and consumers to see the impact of the fall in oil, energy and other input prices and if these are being passed on down the chain. The market conditions in the UK are very tough at the moment. Competition is as fierce as it has ever been. All of the leading retailers are looking to emphasise good value for money. Falling oil and energy prices provide part of the backdrop. The role of the GCA is another part of the jigsaw.

Will we see this take place? We will have to wait and see. The impact of the falling price of oil might well further drive competition between the major players at the point of sale and their suppliers. This might see new twists and turns as to how supply chain relationships will evolve. Maybe the only clear winners are likely to be consumers, with food producers, retailers and foodservice companies almost falling over to serve them and gain their custom.

• Emma Hancocks is a senior consultant at Promar International and oversees bespoke "dashboard" reports focused on understanding and forecasting trends within the UK and international food industry. She is also the current holder of the BIAC Young Agricultural Consultant award. She can be contacted at the following email: emma.hancocks@genusplc.com.