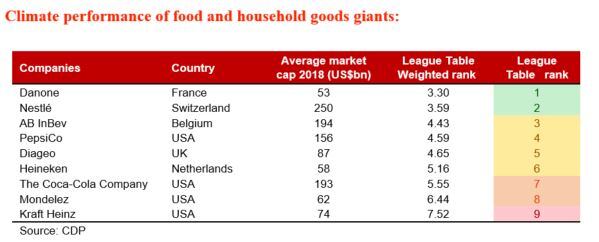

In a report out today, Fast Moving Consumers, environmental non-profit investment research provider CDP ranked nine of the largest publicly listed food and beverage companies on their business readiness for a low carbon transition. Danone and Nestlé came out top – Mondelez International and Kraft Heinz ranked bottom.

“We wanted to look beyond product innovation to include an analysis of both process and systems level innovations. While incremental product innovations have historically been sufficient to keep ahead of the market, we now see consumers demanding more transformative innovations that require fundamental shifts in business models,” Christie Clarke, research analyst at CDP and co-author of the report, told FoodNavigator.

To achieve this, CDP assessed low carbon innovations using a transformative change theory, which Clarke said allowed the analysts to categorise innovations as being either “incremental, radical or transformative”.

She explained: “Incremental innovations are those associated with small decarbonisation impacts resulting from minor efficiency improvements or subtle product redesign. Transformative innovations are those that drive system-level changes resulting in significant decarbonisation impacts."

Investment in meat-free, organic and plastics

CDP found some of the most transformative low carbon innovations delivered by the largest listed food and beverage makers focused on the development of vegan and organic product ranges. The investment advisory found five out of seven F&B companies that originally offered dairy- or meat-based products are innovating with vegan alternatives. Clarke pointed to the launch of Unilever's vegan Love Beauty and Planet brand and its organic Knorr range as well as Nestlé's organic Gerber baby food range as examples of innovation in this area.

Growing consumer demand in this category sits at the intersection of concerns about personal and planetary health, Clarke continued.

“Increasing transparency around health and environmental impacts have been enabled by big data and the rise of social media, driving the emergence of the environmentally ‘conscious consumer’.”

Indeed, data from Bloomberg Intelligence shows that annual global sales of plant-based alternatives have grown by double the rate of processed meat since 2010. However, Clarke said, if this trend is to tip to the mainstream and achieve “significant scale” more education is required.

“One barrier to consumers understanding the link between meat consumption and emissions is the complexity involved in calculating their Scope 3 emissions, which are those outside the direct operations of a company and which cover the full life cycle of emissions attributable to a company’s process or product. Scope 3 emissions reporting is generally strong for the sector, however the methodologies used vary in robustness across companies.”

In the future, updated European regulations could increase transparency in this area. “EU regulators are currently working on labelling regulations which could require these lifecycle emissions figures to be displayed on packaging, driving improvements in Scope 3 calculations and providing consumers with more information on which to base their purchasing decisions.”

CDP also described a “tide of consumer activism” on plastic packaging, which has resulted in increased scrutiny and changing preferences for circular, zero-waste business models.

This has prompted companies to rethink their approach to packaging, with around 60% of investing to advance biodegradable plastic and recycling infrastructure. French dairy giant Danone is “leading the way” in this area.

Big brands remain defensive

Despite these developments, large brands within the portfolio are failing to invest in carbon innovation. Almost 60% of the top ten revenue generating brands for each company failed to deliver low carbon innovations in the last ten years, CDP found.

This is significant because the majority of companies included in the study – 88% - generate over 50% of their revenues from these key brands, including Nescafé, Budweiser and Dove.

Rather than innovating themselves, the research found many CPGs are instead acquiring smaller, sustainable brands: 75% of companies have directed M&A efforts towards the acquisition of niche environmental brands over the past five years – more than quadrupling activity.

However, CDP warned, this approach will not be sustainable if their fundamental business models - which are based on driving more consumption - remain unchanged.

“It is important that companies drive these kinds of innovations at group level to deliver scale but also through their core brands to protect brand value,” Clarke argued.

Further risks

Failing to deliver transformative innovations is not only a risk to brand value and reputation. It also threatens to leave companies under-prepared for more robust regulations governing issues like plastic waste.

The EU 94/62 directive’s 2018 amendment has set measures for reducing packaging waste at source as well as improving recycling and recovery, while product labelling and carbon footprinting is on the horizon.

The sector is also highly exposed to the physical risks associated with climate change, which has the potential to disrupt agricultural supply chains and cause price volatility. “This poses a real threat to the sector, especially for diversified food companies like Nestlé and Kraft Heinz that rely on a variety of raw materials.”

‘Drive innovation at scale’

The current food system, which relies on “low-cost, high impact production”, is being called into question as consumers increasingly expect traceability and seek out meat-free and organic products.

For food and drinks companies, carbon impacts are heavily weighted upstream in agricultural supply.

“Aligning with these changing consumer preferences and actively engaging with suppliers to manage supply chain risks offers the biggest wins both from a low carbon perspective and from a business resilience perspective,” Clarke suggested.

A call to action

Clarke shared the top three actions food makers can take to transition to low carbon models.

1. Collaborate across the value chain – “Given the inherently systemic nature of the global climate challenge and the fact that around 90% of the consumer goods sector’s emissions lie in the value chain, it is critical that consumer goods companies engage both upstream with their suppliers and downstream with their consumers to drive meaningful decarbonisation.

“This will open up opportunities for companies that do so. The sector’s close proximity to the consumer gives companies the ability to engage directly with their consumers and drive behaviour change to shape the markets into which they sell, ensuring the longevity of their brands. Supply chain engagement will also help to build resilience and ensure a secure supply of key commodities as climate impacts on agriculture begin to intensify.”

2. Embed circular principles where possible – “Today’s consumer goods sector is inherently linear, reliant on a single use culture which has been pervasive for several decades. But things are changing. Consumers are increasingly demanding products with lower packaging footprints and circular models for product deliver. Many FMCGs have responded to this by pledging to make their packaging recyclable but given current recycling rates and the absence of adequate recycling infrastructure in many emerging economies, this is not enough.

“Transitioning to a circular economy for all packaging through models such as refillables, take-back schemes and increasing the use of recycled content would not only align businesses with emerging consumer preferences but also drive decarbonisation benefits.

“While packaging is the key area where circularity can be applied, companies should work to identify other opportunities to embed circular principles throughout the value chain. For example, using the by-products of manufacturing processes to produce biofuels or feedstocks for agricultural suppliers or engaging with consumers on food waste.”

3. Drive innovation at scale – “While 15 out of 16 of the companies [F&B plus home and personal care] we assessed have delivered transformative innovations, these tend to be deployed at a small scale and are generally experimental in nature. Only 14% of transformative innovations have been rolled out at group level. For innovations to really drive meaningful, decarbonisation impacts that must be scaled up and integrated across the business.”