From Mr Kipling and Cadbury cakes, to Bisto and Angel Delight, Premier Foods is the home to some of the UK’s most recognisable national brands. But the food maker is plagued by historic borrowing and pension liabilities, which are so high that some of its largest investors have described the Bisto-to-Mr Kipling maker as a “zombie company”.

Drowning in debt

In the early 2000s, the group went on a debt-fuelled acquisition spree of businesses including the UK and Irish unit of Campbell Soup Co., the owner of the Hovis bread brand Rank Hovis McDougall (RHM), the UK ambient dessert business of the then Kraft Foods, as well as meat-free brands Quorn and Cauldron Foods. Pension liabilities for former and existing employees added further still to what was rapidly becoming an unassailable financial burden.

Overextended and overleveraged, this situation was clearly unsustainable: In the next decade, Premier began selling off assets. Disposals included an array of brands like Quorn, Crosse & Blackwell, Branston, Hartley’s and Sun Pat as well as the spin-off of the Hovis bread business.

CEO Gavin Darby joined Premier at the beginning of 2013 – when net debt stood as a massive £831m. He was responsible for overseeing much of the restructuring that took place. Under his stewardship Premier introduced a new capital structure - an underwritten equity issue of approximately £353m, a new pension schemes agreement, a high yield bond of £500m and a new lending agreement with a smaller banking group.

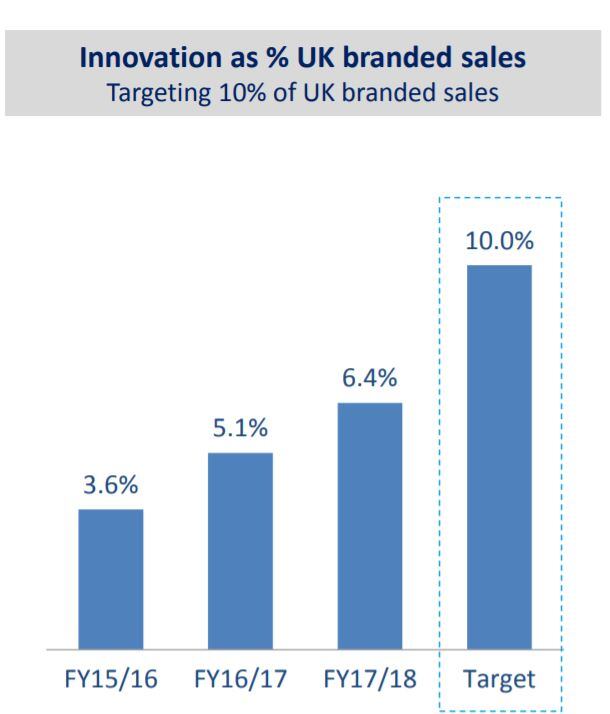

Debt limited scope for investment

The company rolled up its sleeves and focused on paying down its debt. Premier aims to cut net debt to below 3xEBITDA. In an earnings release this morning, Premier revealed net debt was cut to £509.5m in the first half of the year, compared to £535.3m in the prior year.

At the same time, the group attempted to support organic sales trends through innovation, increased private label production and international expansion. Premier has simultaneously forged partnerships with global players, such as Mondelez International in cakes and Nissin in noodles.

Premier is targeting a 10% contribution from new products to total sales. In fiscal 2017/18, this stood at 6.4%.

This strategy meant Premier was also able to report positive underlying trends for the first six months of the year. On sales growth of just 1.3%, to £358m, Premier said trading profit increased 6.2% to £51m in the half.

This was achieved in an operating environment that is somewhat challenging. The group is grappling with input cost inflation, an ongoing channel shift that has seen shoppers gravitate to the discounters where Premier’s brands have limited exposure, and food price deflation driven by a price war in the UK’s largest supermarkets.

Despite an improving operating result, Premier’s massive debt levels mean that the company continues to hemorrhage cash in terms of financial expenses to service its borrowing. Financial expenses, including write-downs, totalled £32.9m in the six-month period, dragging the group into the red. Premier reported a net loss of £0.7m.

The discipline needed to pay down debt also meant that the company’s ability to invest in marketing and brand building is limited.

“The leverage in Premier still dominates the investment thesis and the recent-rate of pay-down is too pedestrian to eat into its indebtedness to the point that the group can be less inhibited and, for example, recommence dividend payments, more substantially support its core brands or use its paper for earnings enhancing M&A activity,” Shore Capital analyst Clive Black noted.

Under-fire Darby departs

Premier’s progress – or lack thereof – has provoked the ire of some vocal investors. Just four months ago, Darby saw off an attack from Hong Kong based activist investor Oasis Management – the company’s second-largest shareholder - which called for his removal.

Oasis wanted Premier to sell off its Batchelors soup brand, which it believed could be worth around £200m. Unusually perhaps for an activist investor, the group called on the proceeds to be used to de-risk the business, not returned to shareholders.

Oasis did not pull its punches, describing Darby’s tenure as marked by “years of persistent shareholder value destruction, poor financial performance, consistent[ly] missed targets, a lack of strategy and weak corporate governance”.

ShoreCap’s Black is considerably less damning in his assessment of Darby: “Under his tenure Premier Foods has become a demonstrably more effective operator and it has made commendable progress with brand development.”

The majority of Premier’s shareholders and the Premier board agreed: Darby survived the AGM vote in July. But fast-forward to today, and it seems Oasis might be getting roughly what it wanted.

The Bisto maker revealed that its board will begin a search for a new chief executive, with Darby standing down on 31 January – his six year anniversary. Premier is also working on the sale of its Ambrosia business.

"While we are committed to our strategy of improving operating performance and targeting a bet debt to EBITDA ratio below 3x by March 2020, we are also working in parallel to identify other strategic opportunities to accelerate the company's turnaround,” Darby commented.

“The board has determined that it should focus resources on areas of the business which have the best potential for growth through accelerated investment in consumer marketing and high return capital projects. Accordingly, we are pursuing options to fund these plans as well as delivering a meaningful reduction in net debt, through discussions with third parties regarding the potential disposal of our Ambrosia brand.”

Will it be enough?

Premier’s debt levels have come down, but this latest announcement recognises that organic reduction is not a sustainable option.

The sale of Ambrosia makes sense logistically, Jefferies analyst Martin Deboo suggested. It will be relatively easy to carve out the brand, which is produced at a single factory. However, with sales of £90m, the brand would have to fetch a high multiple if it is to move the needle on Premier’s indebtedness.

“The exit multiple will have to be high single digit EBITDA to drive meaningful deleverage,” Deboo said.

In Greek mythology, Ambrosia is the nectar of the Gods associated with life and vitality. It seems fitting that Premier is pinning its hopes of shedding its zombie status on the brand. However, with Brexit uncertainty casting a shadow over the M&A landscape, it is far from certain that Permier's troubles are over.