Sainsbury’s and Asda – the UK’s second and third largest supermarkets – have reached a merger deal that would see the creation of a retail giant with combined sales of around £51bn (€58bn). If the agreement gets the go-ahead from competition authorities, the enlarged entity would leap-frog Tesco to become the UK’s largest grocery retailer by market share.

US retail behemoth and Asda owner Wal-Mart – known for its cut-throat supplier negotiations – would hold 42% of the issued share capital and the combined business would receive £2.975bn in cash, valuing Asda at around £7.3bn. Wal-Mart will be a “long-term partner”, with almost 30% of share voting rights and two board seats upon completion.

Providing detail on the news this morning (30 April) alongside its full-year financial update, Sainsbury’s said that the combination would continue to operate its store network of 2,800 outlets under both the Asda and Sainsbury’s fascias. This will enable the Sainsbury's and Asda brands to “sharpen their distinctive customer propositions and attract new customers”, management said.

“This is a transformational opportunity to create a new force in UK retail, which will be more competitive and give customers more of what they want now and in the future,” Sainsbury’s CEO Mike Coupe commented.

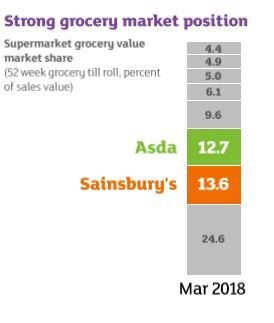

Sainsbury's and Asda are currently the second and third largest grocery retailers in the UK, data provided by the companies at this morning's analyst meeting revealed.

Price cuts planned

The merger is a response to the pressures shaping the UK retail scene.

Sainsbury’s and Asda have been squeezed by the growth of the German discounters, Aldi and Lidl. Sainsbury’s has found its more up-market positioning under pressure from the likes of Waitrose, particularly in its southern heartland. While Asda’s big box out-of-town stores have been losing ground as consumers increasingly shop online or at local, smaller supermarkets.

These forces have combined to deliver a highly competitive environment where shoppers expect supermarkets to deliver on both price and quality.

Speaking during an analyst meeting this morning, Coupe argued that the merger proposition has been developed as an answer to these challenges. “We will create a more dynamic, more adaptable, more resilient business. For customers that will result in lower prices, better quality, differentiated ranges and more flexible ways to shop.”

Through the merger, the enlarged retail group is targeting a 10% cut in the price of everyday essentials, Sainsbury’s revealed. This is on top of the investment Sainsbury’s and Asda are already making in price. In the year to end-March, Sainsbury’s invested £150m in lowering prices, the group stressed.

“We can see our way to reducing every day items buy 10%...That is above and beyond investments both businesses are already making in price,” Coupe commented.

Buying synergies

Significantly for suppliers, Coupe said management expects the combined company would deliver significant buying synergies.

Sainsbury’s said it expects net synergies, after investments in the customer offer, to total £500m two years after completion. The lion’s share of these savings - £350m - will come from buying synergies “primarily focused” on the grocery business.

“All you have to believe, to believe this figure, is that the best terms for either of the companies will be applied for the overall buying book. It does not take into account any volume benefits that may be accreted,” Coupe noted.

This therefore makes it likely that suppliers will come under pressure to deliver better terms and lower prices.

“The supply chain will be quite guarded with respect to this proposed deal,” Shore Capital analyst Darren Shirley noted.

Shirley told FoodNavigator that procurement savings are expected from both branded and private label suppliers.

‘More opportunity’ for suppliers?

Nevertheless, Coupe insisted that the tie-up represented a win-win, arguing that suppliers would be able to leverage more efficient supply chains and access to a larger store base.

“We think it’s a great deal for everyone,” Couple said. “For suppliers we will offer greater efficiency, we will offer the opportunity for differentiated ranges and through the combined entity the opportunity to grow into the future.

“There is a great op to grow with a larger business. Streamlined supply chains mean more efficiency as far as suppliers are concerned. Both businesses have heritage of bringing new and differentiated products to market, and we will protect choice for customers in the future.”

Shirley, however, believes that the only way suppliers will benefit is if the combined Sainsbury’s-Asda business is able to deliver market share growth. “Unless share gains through volumes can be generated, then we sense that there will be a circumspect and cautious supply industry,” he noted.

Will market share expansion follow?

Whether Sainsbury’s and Asda will be able to deliver market share gains is another question.

Sainsbury’s results for fiscal 2017/18, also reported today, came in a little ahead of market expectations, with underlying profit of £589m. However, guidance for the coming 12 months was somewhat subdued.

While the group’s grocery sales have stood up relatively well over the last decade, the grocery business is underperforming the market in the face of continued growth at Aldi and Lidl and a demonstrable uplift at Tesco and Morrisons. According to market share figures from Kantar Worldpanel, Sainsbury’s share of the market dropped to 15.8% in the 12 weeks to 25 March, down from 16.2% in the prior period to the 25 February.

Asda, for its part, is moving towards stabilising its sales after five years of under-performance. The company has been hit by a significant decline in its market share, but in the most recent period was able to stabilise this at 15.6%, Kantar data revealed.

“We have momentum in the business, we have our mojo back,” Asda CEO Roger Bernley argued this morning. He attributed improvements at the group to its everyday low price strategy and pricing investment – again pointing to the likelihood of increased price focus moving forward. The company also reformulated “more than 1400 own label products” last year, the chief executive noted.

Coupe added the joint business will have a strong footprint in the faster-growth spaces of UK retail: digital and convenience.

Sainsbury’s and Asda will benefit from a “strong, fast-growing online business” as well as highly developed “in store technology” to ease the path to purchase. Sainsbury’s Local stores will continue to be an important part of the group’s growth strategy, the executive confirmed. The company currently operates more than 800 Sainsbury’s Local outlets with what he termed “market leading sales densities” and a “record of growth”.

Shirley is not convinced that the combined Sainsbury’s and Asda will be able to turn around the trends we are seeing in their market shares.

“The combination from a growth perspective in grocery does not appear overly compelling to our minds. Rather, it looks like two organisations that are struggling to compete have decided that it is better, or easier, to combine with one-off synergies, than go head to head; the two drunks propping each other up characterisation is hard to strip from the mind,” he suggested.