Slow growth

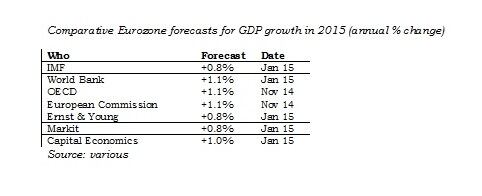

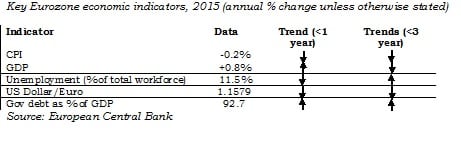

Growth in the Eurozone in the first three quarters of 2014 faded away in Q4 and, with it, confidence that the economy was on a path to sustainable growth. With concerns over falling consumer prices (the Consumer Price Index – CPI) which is currently -0.2%, high unemployment, high government debt and unresolved structural issues between member states, most economists have recently cut their forecast for 2015 and are now predicting GDP growth of between 0.8% to 1.1%.

Buying time

The European Central Bank (ECB) has implemented a new monetary policy strategy (quantitative easing, or QE) to attempt to stimulate growth by purchasing €60 billion in asset-backed securities every month until the end of September 2016. The total QE package could be as much as €1.1 trillion and, it is hoped, that this injection of money into the Eurozone economy will encourage banks to lend more money to businesses and to private consumers.

On the back of a poor economic data and the announcement of the ECB’s QE programme, the value of the euro has fallen, particularly against the pound sterling and US dollar. This will have two effects. First, a weak euro will temporarily boost the competitiveness of Eurozone exports and will therefore encourage growth – good news for countries such as Denmark and the Netherlands, maybe, and other EU export sources. Secondly, it will also mean imports into the Eurozone will become relatively more expensive and could dampen demand. This could, as an example, affect meat imports from the likes of Brazil, Argentina, the US, Canada, Thailand, New Zealand and others outside the Eurozone.

Contrasting fortunes

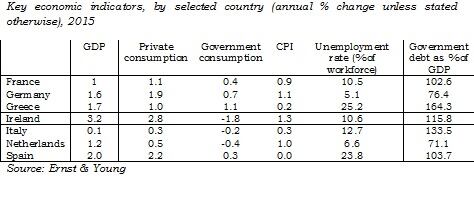

Maintaining unity within the currency union has always been difficult, given the mix of stronger and weaker member states. This is even more so with the polarisation in fortunes between the stronger, northern European countries and the weaker southern European countries.

• Greece has not reduced its debt burden (164% of GDP) and unemployment is still very high at 25.2% of the workforce.

• Spain has similar problems; government debt is high (103.7% of GDP), as is unemployment (23.8% of the workforce). However, economists tend to be more bullish about the prospect of a private sector-led recovery, leading to economic growth of 2% in 2015.

• Italy is the largest of the Eurozone economies to continue to be troubled by high government debt, high unemployment and little/no prospect of growth in 2015.

• Germany continues to be the strongest Eurozone economy, with robust GDP growth led by private sector consumption, low unemployment and manageable government debt.

• The outlook for France is that private sector consumption will lead to growth of around 1% (on a par with the Eurozone as a whole); however, it still must deal with high unemployment and government debt.

A welcome break for consumers?

Despite considerable uncertainties in the Eurozone economies, the prospects for some consumers may be improving, at least in the short-term. The prevailing rate of interest set by the ECB is 0.05% and, given weakness in the Eurozone, a rate rise in 2015 seems unlikely. Low interest rates will help to keep borrowing costs down, especially for mortgages – most households’ biggest expenditure item. More recently, a fall in the oil price (and prospect of low prices in the short-term) has led to a fall in fuel prices. Moreover, according to the FAO Food Price Index, global meat prices are now at their lowest level in four years.

Impact on food expenditure

We would anticipate the improvement on household budgets, caused by falling fuel, energy and food bills, to have a positive effect on food expenditure. This includes meat. However, this effect is only likely to be moderate, as it will be constrained by the low growth felt across the Eurozone as a whole.

The economic environment of the past five years – not just in the Eurozone, but in most developed economies – has led to a change in food purchase and consumption behaviours that will be slow to change. Therefore, we largely expect many current behaviours will continue to play out; for example:

• Growth at the discount end of the retail market. We expect the appeal of the discount retail chains will continue to build in 2015, particularly for fresh meat products.

• Growth at the premium end of the retail market. We expect consumers to continue to be motivated to purchase affordable indulgences. This is likely to benefit categories such as meat-based ready meals

• Price sensitivity. Consumers have undoubtedly become more aware of, and sensitive to, meat and other food prices.

• Growth in out-of-home consumption. Meat products eaten out of the home are sensitive to changes in the economy and, with an improved outlook for the consumer environment, we expect to see moderate growth in out of home consumption

• Everyday low prices. Consumers increasingly perceive volume-driven promotions – for example, buy one pack, get one free – to lead to unnecessary waste, especially in fresh meat categories and therefore poor value for money.

Conclusion

The Eurozone is not without its difficulties and the outlook for 2015 suggests growth will be modest at best. However, despite the less-than-optimistic short-term economic outlook, the Eurozone still holds major attraction. It is the largest trading bloc in the world and is home to 335 million consumers, with an average GDP per capita of US$32,152 (PPP terms). It is also home to many world-class retail customers and has an efficient and well-functioning infrastructure. It has always been the case that some countries within the Eurozone are better opportunities than others. This is more likely to be the case now, than ever before and we would recommend a strategy for meat processors and exporters that targets specific countries, rather than the region as a whole.

Matt Incles is a senior consultant with Promar International, the value chain consulting arm of Genus plc, and a specialist in international food markets. He can be contacted at the following email address: matt.incles@genusplc.com